Updates to 2023 Medicare IRMAA

Good news for retirees and Medicare recipients: For the first time in about a decade, premiums for Part B have decreased by about 3% in 2023. One area not often considered, however, is how much is paid into Medicare Part B and Part D monthly premiums. The amount you pay is based on your Modified Adjusted Gross Income (MAGI), which is your total adjusted income plus tax-free income from municipal bonds. Income-related monthly adjustment amount (IRMAA) is an additional surcharge you pay on top of your monthly premiums, and it is assessed based on your MAGI from two years ago. So, for 2023, your IRMAA is based on your MAGI from 2021.

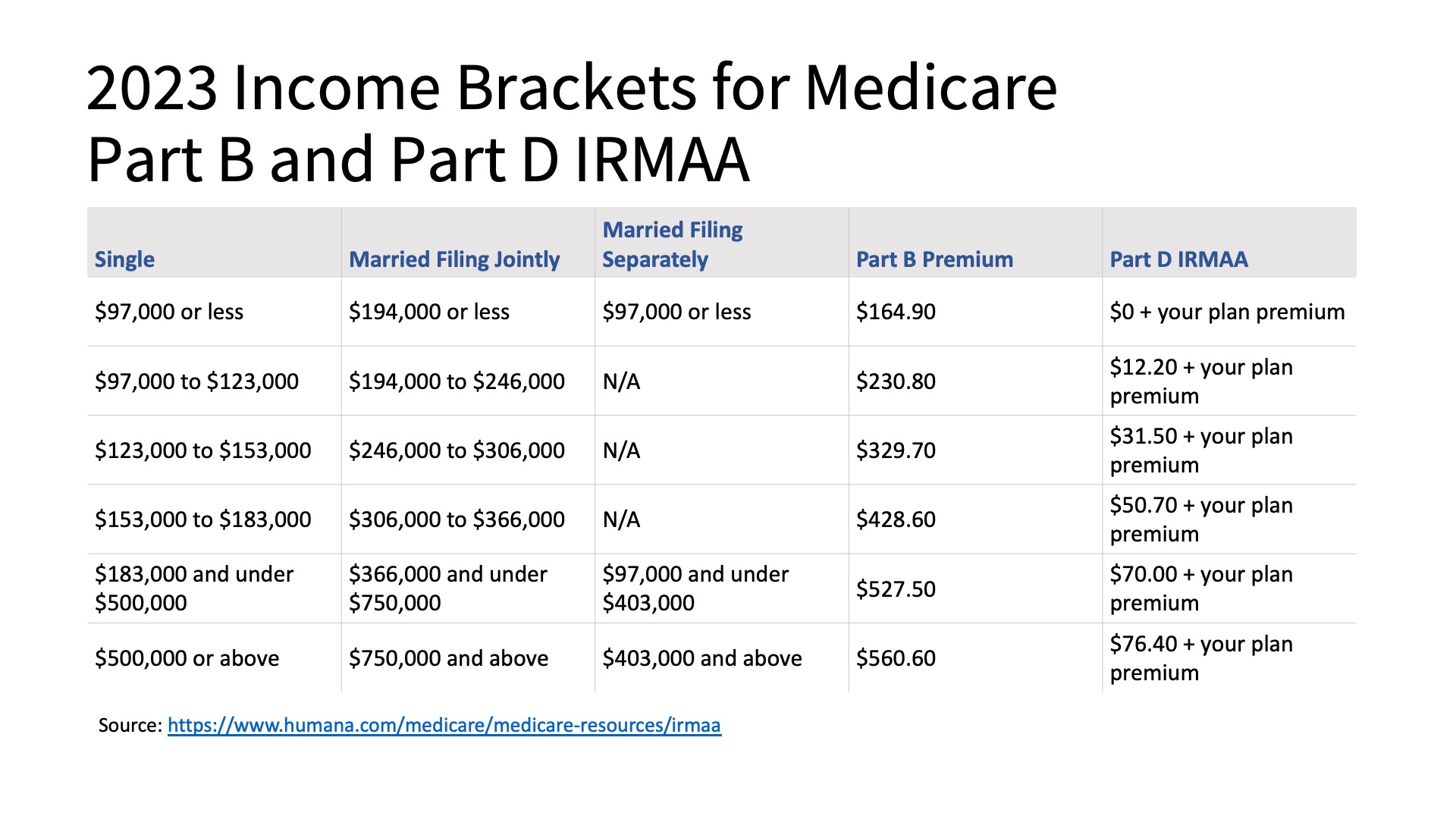

An example of how IRMAA works

Let’s say that in 2021, you sold your home as a single filer earning $500,000 or above, or you are married filing jointly, earning $750,000 or above. Those incomes would place you (or you and your spouse) into the highest IRMAA Medicare brackets. For Part B, your monthly premium would be $560.60, and Part D would cost $76.40, per Medicare recipient.

Why IRMAA is important for tax planning purposes

While your Medicare premiums may increase because of the two-year outlook, remember that they will reset. Using the previous example, if it was a normal income year for you (you didn’t have a large taxable event, like selling your home), your income as a single filer was $97,000 or less, or you filed married filing jointly earning $194,000 or less, your bracket would place you at a monthly premium of $164.90 for Part B and $0 for Part D.

Now, presumably, you wouldn’t be selling a home every year, but this is why tax planning and projection are important. Current IRMAA bracket limits are wider than they were before, but you want to be prepared for Medicare premiums to jump if you’re considering selling stock, taking a large IRA distribution, or converting to a Roth IRA – anything that could possibly contribute to an increased income tax bracket.

Preparing for Medicare IRMAA brackets in 2023

If you have any questions about how Medicare premiums or IRMAA brackets might affect your tax or retirement planning this year, please contact us. Our financial advisors and tax professionals will discuss your options with you and help you make proactive financial decisions, so you’re not left with any surprises come tax time.

Sincerely,

The Team at Chatterton & Associates

Although the information has been gathered from sources believed to be reliable, it cannot be guaranteed. Federal tax laws are complex and subject to change. This information is not intended to be a substitute for specific individualized tax or legal advice. Neither Royal Alliance Associates, Inc nor its representatives provide tax or legal advice. As with all matters of a tax or legal nature, you should consult with your tax or legal counsel for advice.